February 2022 Newsletter

Volatile Times

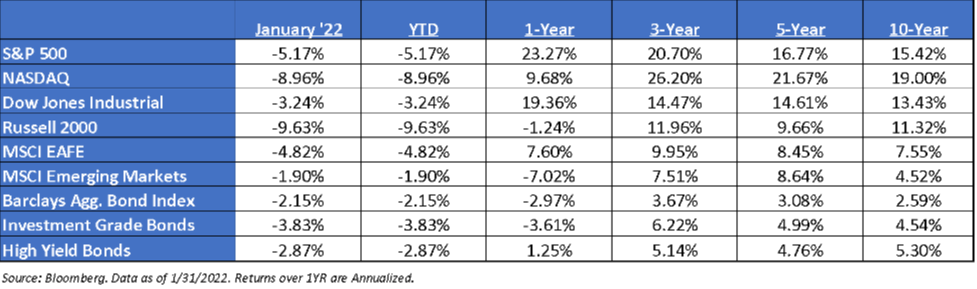

Wow! What a roller coaster of a month January was from a market perspective. The S&P 500 and the Nasdaq Composite posted their worst months since the onset of the pandemic, as investors braced for the Federal Reserve to raise interest rates multiple times this year.

- S&P closed at 4,515 (-5.3% for the month)

- Dow Jones Industrial Average closed at 35,131.86 (-3.3% for the month)

- Nasdaq Composite closed at 14,239.88 (-8.9% for the month)

At the end of January, the Fed indicated that it will likely start raising rates in March to combat historically high inflation. That would be the central bank’s first rate hike in more than three years. Markets are now pricing in at least 4-5 rate hikes in 2022. On top of raising interest rates, the Fed has also announced the end of Quantitative Easing (QE) by tapering its bond purchases later this year. There has even been tough talk from the Fed about Quantitative Tightening in 2022 to reduce its balance sheet. In essence, the Fed is hinting that the money printing and liquidity are about to stop and that they will actually start to go in the opposite direction by tightening the money supply. We are under the opinion that the markets have not fully priced this in and if the Fed does follow through with tightening, you could expect volatility to continue throughout most of the year.

There is good news heading forward, however. At Abraham & Co., Inc. we don’t believe in the Old Wall Street mantra of “Just Ride it Out.” We believe in taking a more proactive approach when it comes to money management. Beginning in early January, we started to make the pivot out of our growth models, into more conservative models to weather the impending storms that are headed towards the markets (and your hard-earned money). As a result of this pivot, our models have held up remarkedly well to this market volatility. We anticipate that January was just a preview of what is in store for the markets. The analysts we rely on for forecasting, are anticipating a “deep Quad 4” by the second quarter of this year. They see the Fed raising interest rates and tightening just as the US Economy begins to decelerate. So far, this theory is being supported by the data that is coming out of the most recent economic data. On top of that, we are heading into the toughest year-over-year comparisons for most businesses. Translation, most stocks are going to miss earnings and will have to adjust their forward guidance towards the downside. This will most likely lead to even deeper bear market conditions.

Here is what we are covering in February’s newsletter:

- Market Updates – Rearview to Windshield

- Analysts Updates – Quad update

- Tax Documents from TD Ameritrade

- Social Media updates (website, LinkedIn, Facebook, and YouTube)

This Month’s Advisor Spotlight – Kyle Appelbaum (Spokane office)

Kyle Appelbaum comes to us from US Bancorp Investments and is the newest addition to our team at Abraham & Co. He is a fiduciary financial advisor with over 5 years of experience in the financial industry and is excited to assist Darrin in providing our firm’s top tier client experience.

Kyle was born and raised in West Palm Beach, Florida with his brother. After adventuring to California as a young adult, he then made the move to Spokane in 2015 because housing costs were cheaper and he found a new opportunity with US Bank. His decision to delve into finance came from the desire to help his parents and his friends with their investments.

Outside of the Abraham and Company firm, Kyle has many hobbies here in the Spokane area such as snowboarding, motorcycle racing, and mixed martial arts. He and his fiancé’, Deziree, will be getting married in December 2022 and will be settling down in right here in Spokane Valley.

Market Updates – Rearview to Windshield

Monthly Recap:

We’ve seen big moves in equities to start the year. This has been the worst January for the S&P 500 since 2009 while at the same time it’s been the best start to the year for Value stocks in decades. We expect market volatility to remain high and headline-driven for a while longer.

Enter Volatility:

The new year is certainly off to a volatile start. The huge month-end rallies continued a trend of big swings that has defined markets since the Federal Reserve signaled its intention to tamp down inflation that had swelled to the fastest since the early 1980s. In one session, the Nasdaq 100 erased a loss of almost 5%, while the S&P 500 staged three straight days with swings that topped 3%. Markets are finding themselves in a tug of war between strong earnings and economic growth, and the specter of the Fed raising rates. And not to mention a normalization of egregious valuations.

Equity Fundamentals are Normalizing:

As equity valuations come under scrutiny amid the rapid rise in real rates, investor focus will increasingly assess whether earnings growth can continue to lead the market higher. We are focusing on Q4 2021 earnings, which has had a strong start from MSFT and AAPL. As of year-end, the consensus estimates expect S&P 500 EPS to increase +9% in 2022. We believe there is upside to consensus estimates but expect the frequency and magnitude of EPS beats will moderate from 1H 2022. There remain a few key risks to watch: (1) Supply chains, (2) oil, (3) labor costs, (4) Fed tapering cadence, (5) Omicron variant effects, and (6) China growth.

The Fed Update:

During the January meeting, the Fed did nothing to contain market expectations to four (4) rate hikes this year, effectively inviting the market to price in even more, hence why the market saw a swift move. Furthermore, Powell also hinted that he will be revising up his 2022 inflation forecast, which will pressure the dots higher. Thus, the March SEP is likely to show four (4) hikes at a minimum, and possibly more (up from three in December). Fortunately, the FOMC’s balance sheet guidance was a bit more dovish, i.e., helpful in cutting the tail risks. The Fed intends to shrink the balance sheet in a “predictable manner” and “primarily” through runoff, which makes asset sales very unlikely in the first year.

Rate Hikes:

At the same time, market participants are pricing in the potential for as many as five rate hikes by the Federal reserve this year, with some looking for the first hike in March to be 50 basis points. We continue to think that the hawkish estimates will prove to be overblown. The current Federal Reserve has been both hyper transparent, and steadfastly deliberate in their actions. The potential for them to do anything that surprises the markets seems unlikely.

Yield Curve Flattening & What It’s Telling Investors:

The yield curve’s flattening is a sign of growing concern that the Fed is going to hike too much and break something. The curve is not inverted, which would signal the market believes things are already breaking, but it is rapidly moving toward that level. As the short end of the curve rises, so too do the odds of rate hikes. The market has five (5) rate hikes priced in by the end of 2022. A sixth hike is priced in by March 2023. The market still sees the terminal rate settling in around 1.75% or 2.00%.

Fourth Quarter Earnings Season Has Begun:

Fourth-quarter earnings season has been constructive. So far, earnings growth is coming in at 25.3% year over year, with companies in aggregate reporting earnings 4.1% above expectations. That’s in line with the long-term average beat rate, but well below the 16% average beat in the previous four quarters. Companies that have reported growing profit margins in the quarter have seen their stocks rise about 1% the next day, on average, with those that beat earnings climbing 1.4% and those that missed slipping 1.6%.

Earnings:

2021 S&P 500 operating earnings = $209. 2022 = $224. 2019 = $165. Bottoms-up for 2020 = $142.

Valuations:

S&P 500 Fwd. P/E is at 20.3x. EAFE is 14.3x forward P/E, while EM is at 11.7x. R1V is 15.9x v. R1G at 27.1x.

Talking Points – February 2022:

- Though it wasn’t passed in 2021, President Biden outlined the biggest expansion of the federal government matched with the largest tax increase since 1968. Biden senses the post-COVID era is a once-in-a-generation opportunity to massively restructure US fiscal, monetary, and social policy. In our opinion, this is a big experiment. We’ll wait to see how the Build Back Better plan and taxes pan out. It appears that this dramatic change in societal direction has proved to be difficult for some moderate Democrats to get on board, i.e., Manchin.

- We have expected bond yields to reflate as the pandemic improves and economic activity begins to normalize. The spread on the 2s and 10s has historically expanded as wide as 300 bps (~73bps as of January month-end). This year’s peak was in March at ~160bps. Real Rates have never been negative outside some sort of Quantitative Easing environment.

- This past year was led by a bunch of one-hit wonders, i.e., most likely not repeatable – a very dovish Fed, a successful economic reopening, and $8T of stimulus. None of which are expected to sustainably pump liquidity into the market next year. In 2022, the market may have to navigate a slew of negative headlines – increased taxes, higher-than-expected inflation, continued supply bottlenecks, and the possibility of more variants. All in all, we believe that this can create an environment of increased volatility.

- We feel it will be worth watching the general trend of economic and fundamental data, and when it will begin to decelerate.

- Longer-term, we believe valuations and bond yields will eventually matter, and both will lower expected returns for balanced portfolios.

Analysts Updates – What the data is telling us

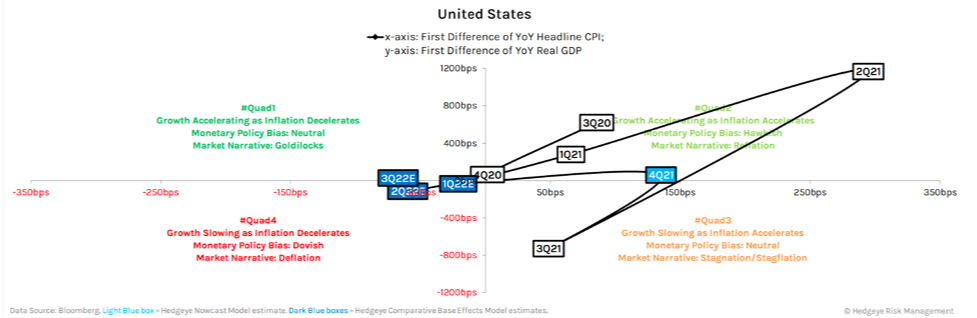

The markets are signaling to the Fed, “We don’t like raising interest rates!!!” Now the Fed and the markets are locked into a game of chicken. Will the Fed really raise rates 5 times in 2022, possibly sending the markets into crash mode? Or, will the Fed tuck tail after the first rate hike and actually cut interest rates to prop up the markets heading into the 2022 mid-term elections? We know that technically the Fed’s job is not to keep the stock markets going up. But, the Fed chairmen are appointed to their positions by political elected officials. There will be tremendous pressure from politicians on the Fed to not crash the markets and ultimately destroy the economy in a critical election year. What will the Fed do? This uncertainty has led to a spike in volatility as most major market indices head for correction territory (-10% or more).

If you examine the chart above, you can see that 2022 is starting out in Quad 4. This is being supported by the recent market declines. The analysts we use are stating that we are headed for “deep Quad 4” in the 2nd quarter of 2022. To keep it simple, this means that the markets will most likely be bearish heading forward. As more data comes in, we will keep you posted by sending out timely market updates via emails and videos from our Chief Investment Officer, Darrin McComas. For the time being, we anticipate staying in our very conservative portfolio models until the economic and market conditions start signaling that brighter times are ahead.

Taxes

Would you like a second opinion on your 2021 taxes before you file them with the IRS? We recently purchased access to an amazing tax planning tool by Holistiplan. With this service, we can immediately identify key income break points for tax planning opportunities like ROTH conversions, tax-efficient withdrawals, charitable giving, and much more. We are offering this service to ALL of our clients 100% FREE OF CHARGE. Before you submit your return to the IRS, feel free to email us a PDF copy of your return and we will run it through Holistiplan’s software and send you a FREE report that will highlight possible missing deductions as well as opportunities to do some tax minimization planning for 2022.

Tax Updates – Tax Documents from TD Ameritrade

To help make sure you receive your tax documents as soon as they are available, please sign up for electronic tax form delivery. You can sign up for e-delivery of tax documents by logging into www.advisorclient.com, then click My Profile > Communication Preferences.

You can find the tax documents on advisorclient.com by simply clicking the appropriate document on the Statements & Tax Documents menu.

We have listed useful information below pertaining to the anticipated dates our 2021 Consolidated Form 1099s will be available to be viewed online.

Thank You for Trusting Us

We would personally like to thank you for trusting Abraham & Co. with your retirement. If you have any questions regarding your accounts or retirement plan, please don’t hesitate to reach out and book an appointment with one of our financial advisors. Expect some choppy markets going forward in 2022, but rest easier that your hard-earned money is being actively managed to minimize drawdowns during these tough market conditions. We are listening to the market analysts continuously and we will continue to make small adjustments to your investments to preserve, protect and grow your retirement savings to the best of our abilities. While no one has a crystal ball and can forecast what the markets are going to do with 100% accuracy, we feel we have access to some of the best macro analysts in the world and with their expert guidance, we will navigate through these choppy markets until smooth sailing eventually returns. Have a blessed February from everyone here at Abraham & Co., Inc.

Disclosures

This commentary offers generalized research, not personalized investment advice. It is for informational purposes only and does not constitute a complete description of our investment services or performance. Nothing in this commentary should be interpreted to state or imply that past results are an indication of future investment returns. All investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with an investment & tax professional before implementing any investment strategy.

Past performance is not indicative of future results. This material is not financial advice or an offer to sell any product. The information contained herein should not be considered a recommendation to purchase or sell any particular security. Forward looking statements cannot be guaranteed.

The S&P 500® is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 11.2 trillion indexed or benchmarked to the index, with indexed assets comprising approximately USD 4.6 trillion of this total. The index includes 500 leading companies and covers approximately 80% of available market capitalization.

The Nasdaq Composite Index measures all Nasdaq domestic and international based common type stocks listed on The Nasdaq Stock Market. To be eligible for inclusion in the Index, the security’s U.S. listing must be exclusively on The Nasdaq Stock Market (unless the security was dually listed on another U.S. market prior to January 1, 2004 and has continuously maintained such listing). The security types eligible for the Index include common stocks, ordinary shares, ADRs, shares of beneficial interest or limited partnership interests and tracking stocks. Security typesnot included in the Index are closed-end funds, convertible debentures, exchange traded funds, preferred stocks, rights, warrants, units and other derivative securities.

The Dow Jones Industrial Average® (The Dow®), is a price-weighted measure of 30 U.S. blue-chip companies. The index covers all industries except transportation and utilities.

The Russell 2000® Index measures the performance of the small-cap segment of the US equity universe. The Russell 2000® Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 2000® is constructed to provide a comprehensive and unbiased small-cap barometer and is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true small-cap opportunity set.

The MSCI EAFE Index is an equity index which captures large and mid-cap representation across 21 Developed Markets countries*around the world, excluding the US and Canada. With 902 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI Emerging Markets Index captures large and mid-cap representation across 26 Emerging Markets (EM) countries*. With 1,387 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. This includes Treasuries, government-related and corporate securities, mortgage-backed securities, asset-backed securities and collateralized mortgage-backed securities. ACA-2201-1.

© 2022 Abraham Co.. All Rights Reserved.

Investing involves risk and potential loss of principal. There can be no assurance that any investment will achieve its stated objectives. TD Ameritrade Clearing, Inc. (“TD Ameritrade”) is the firm that we use to custody our client assets. TD Ameritrade and Abraham & Co. Inc. are separate and unaffiliated firms, and are not responsible for each other’s services or policies. TD Ameritrade does not endorse or recommend any advisor and the use of the TD Ameritrade logo does not represent the endorsement or recommendation of any advisor. Brokerage services provided by TD Ameritrade Institutional, Division of TD Ameritrade, Inc., member FINRA/SIPC. TD Ameritrade is a trademark jointly owned by TD Ameritrade IP Company, Inc. and The Toronto-Dominion Bank. Used with permission.